Պատկեր:Pareto Efficient Frontier for the Markowitz Portfolio selection problem..png

Նախադիտման չափ՝ 800 × 538 պիքսել։ Այլ թույլտվությաններ: 320 × 215 պիքսել | 640 × 430 պիքսել | 1024 × 689 պիքսել | 1392 × 936 պիքսել.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Սկզբնական նիշք (1392 × 936 փիքսել, նիշքի չափը՝ 36 ԿԲ, MIME-տեսակը՝ image/png)

{kind=link}

|

This graph image could be re-created using vector graphics as an SVG file. This has several advantages; see Commons:Media for cleanup for more information. If an SVG form of this image is available, please upload it and afterwards replace this template with

{{vector version available|new image name}}.

It is recommended to name the SVG file “Pareto Efficient Frontier for the Markowitz Portfolio selection problem..svg”—then the template Vector version available (or Vva) does not need the new image name parameter. |

Ամփոփում

| Նկարագրում |

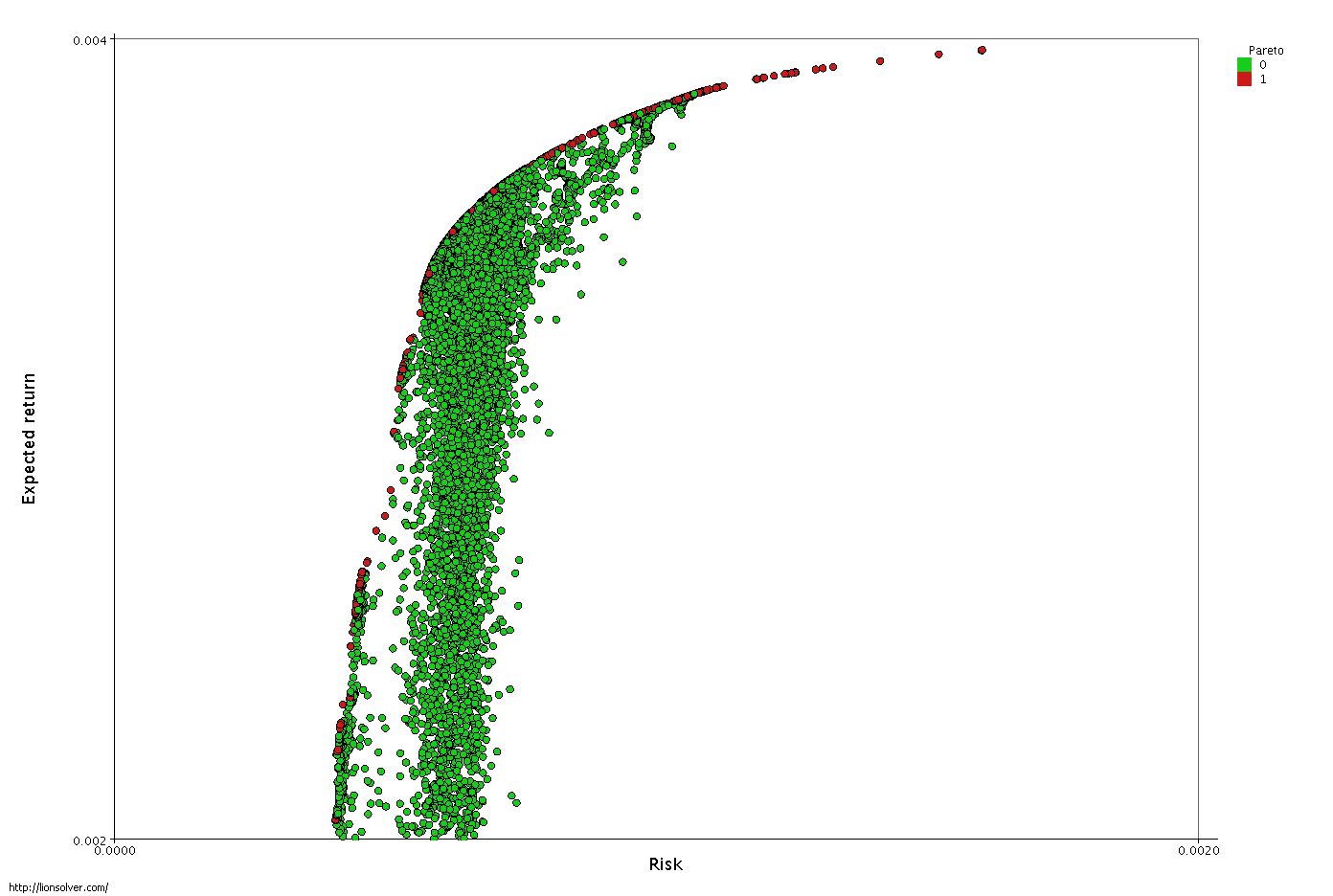

English: The problem consists of selecting a set of assets and choosing the share of investment dedicated to each asset, in order to follow the investor's desires regarding return and risk.

The classic and seminal approach to this problem is due to Markowitz (1952). The plot shows the results of optimizing 225 stocks by using the LIONsolver software, Pareto-optimal solutions are red. ( created with http://LIONsolver.com ) |

| Թվական | |

| Աղբյուր | Բեռնողի սեփական աշխատանք |

| Հեղինակ | Marcuswikipedian |

Արտոնագրում

Ես, սույն աշխատանքի հեղինակային իրավունքների տերը, այսուհետ այն հրատարակում եմ հետևյալ արտոնագրի ներքո։

Այս նիշքը հասանելի է Creative Commons Attribution-Share Alike 3.0 Unported արտոնագրի ներքո:

- Դուք ազատ եք՝

- կիսվել ստեղծագործությամբ – պատճենել, տարածել և փոխանցել այս աշխատանքը։

- վերափոխել – ադապտացնել աշխատանքը

- Պահպանելով հետևյալ պայմանները'

- հղում – Դուք պետք է նշեք հեղինակի (իրավատիրոջ) հղումը:

- համանման տարածում – Եթե դուք ձևափոխում եք, փոխակերպում, կամ այս աշխատանքի հիման վրա ստեղծում եք նոր աշխատանք, ապա ձեր ստեղծածը կարող է տարածվել միայն նույն կամ համարժեք թույլատրագրով։

Նիշքի պատմություն

Մատնահարեք օրվան/ժամին՝ նիշքի այդ պահին տեսքը դիտելու համար։

| Օր/Ժամ | Մանրապատկեր | Օբյեկտի չափը | Մասնակից | Մեկնաբանություն | |

|---|---|---|---|---|---|

| ընթացիկ | 17:36, 29 փետրվարի 2012 | | 1392 × 936 (36 ԿԲ) | Marcuswikipedian |

Նիշքի օգտագործում

Հետևյալ էջը հղվում է այս նիշքին՝

Նիշքի համընդհանուր օգտագործում

Հետևյալ այլ վիքիները օգտագործում են այս նիշքը՝

- Օգտագործումը ar.wikipedia.org կայքում

- Օգտագործումը ca.wikipedia.org կայքում

- Օգտագործումը en.wikipedia.org կայքում

{kind=link}