Պատկեր:U.S. Household Debt Relative to Disposable Income and GDP.png

{kind=link}

{kind=link}

{kind=link}

Սկզբնական նիշք (960 × 720 փիքսել, նիշքի չափը՝ 10 ԿԲ, MIME-տեսակը՝ image/png)

{kind=link}

Ամփոփում

| Նկարագրում |

English: U.S. Household Debt Relative to Disposable Income and GDP 1980-2011 |

| Թվական | |

| Աղբյուր | Բեռնողի սեփական աշխատանք |

| Հեղինակ | Farcaster |

Understanding the chart

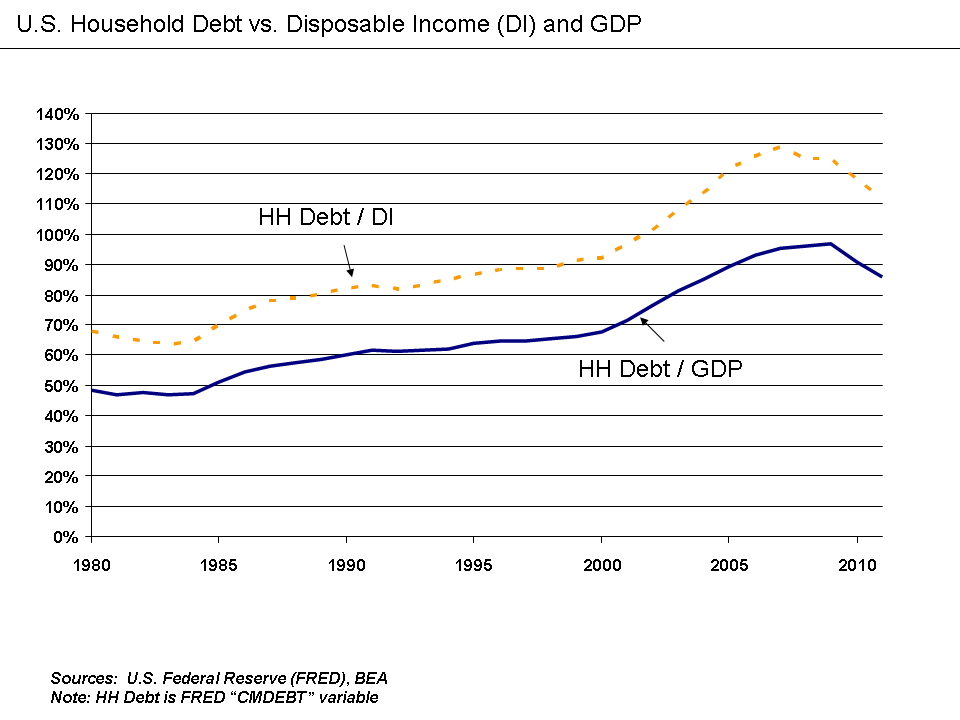

This chart shows how U.S. household (HH) debt (measured by the FRED variable "CMDEBT") rose relative to both GDP and disposable income over the 1980 to 2011 period.

- Household debt as a % disposable income rose from 68% in 1980 to a peak of 128% in 2007, prior to dropping to 112% by 2011.

- Household debt as a % GDP rose from 49% in 1980 to a peak of 97% in 2009, prior to dropping to 86% in 2011.

This chart uses the Federal Reserve Database (FRED) to obtain the CMDEBT variable.[1]

Disposable income data is available from the Bureau of Economic Analysis (BEA).[2]

GDP data is available from the Bureau of Economic Analysis (BEA).[3]

Paul Krugman wrote in December 2010: "The root of our current troubles lies in the debt American families ran up during the Bush-era housing bubble. Twenty years ago, the average American household’s debt was 83 percent of its income; by a decade ago, that had crept up to 92 percent; but by late 2007, debts were 130 percent of income. All this borrowing took place both because banks had abandoned any notion of sound lending and because everyone assumed that house prices would never fall. And then the bubble burst. What we’ve been dealing with ever since is a painful process of “deleveraging”: highly indebted Americans not only can’t spend the way they used to, they’re having to pay down the debts they ran up in the bubble years. This would be fine if someone else were taking up the slack. But what’s actually happening is that some people are spending much less while nobody is spending more — and this translates into a depressed economy and high unemployment. What the government should be doing in this situation is spending more while the private sector is spending less, supporting employment while those debts are paid down. And this government spending needs to be sustained: we’re not talking about a brief burst of aid; we’re talking about spending that lasts long enough for households to get their debts back under control. The original Obama stimulus wasn’t just too small; it was also much too short-lived, with much of the positive effect already gone."[4]

This increase in debt during the period enabled spending that stimulated the economy (arguably hiding the true state of the economy). This debt overhang then began holding back the economy as consumers paid down debt (which reduces economic activity) rather than spend.[5]

During April 2009, U.S. Federal Reserve Vice Chair Janet Yellen discussed the situation: "Once this massive credit crunch hit, it didn’t take long before we were in a recession. The recession, in turn, deepened the credit crunch as demand and employment fell, and credit losses of financial institutions surged. Indeed, we have been in the grips of precisely this adverse feedback loop for more than a year. A process of balance sheet deleveraging has spread to nearly every corner of the economy. Consumers are pulling back on purchases, especially on durable goods, to build their savings. Businesses are cancelling planned investments and laying off workers to preserve cash. And, financial institutions are shrinking assets to bolster capital and improve their chances of weathering the current storm. Once again, Minsky understood this dynamic. He spoke of the paradox of deleveraging, in which precautions that may be smart for individuals and firms—and indeed essential to return the economy to a normal state—nevertheless magnify the distress of the economy as a whole."[6]

References

Արտոնագրում

|

Այս վավերագրման պատճենահանման, տարածման և/կամ ձևափոխման թույլտվություն կամ լիցենզիայի GNU FDL պայմաններով 1.2 մեկնակերպի կամ ավելի ուշ, հրատարակված Ազատ ծրագրային ապահովության հիմնադրամում, առանց անփոփոխելի հատվածների, առանց բնագիրների, որոնք տեղադրված են առաջին և վերջին շապիկներում: Լիցենզիայի պատճենը գտնվում է GNU Free Documentation License հատվածում: |

- Դուք ազատ եք՝

- կիսվել ստեղծագործությամբ – պատճենել, տարածել և փոխանցել այս աշխատանքը։

- վերափոխել – ադապտացնել աշխատանքը

- Պահպանելով հետևյալ պայմանները'

- հղում – Դուք պետք է նշեք հեղինակի (իրավատիրոջ) հղումը:

- համանման տարածում – Եթե դուք ձևափոխում եք, փոխակերպում, կամ այս աշխատանքի հիման վրա ստեղծում եք նոր աշխատանք, ապա ձեր ստեղծածը կարող է տարածվել միայն նույն կամ համարժեք թույլատրագրով։

Original upload log

{kind=link}

- 2012-07-12 12:49 Farcaster 960×720× (10312 bytes) Uploading a self-made file using [[Wikipedia:File_Upload_Wizard|File Upload Wizard]]

Նիշքի պատմություն

Մատնահարեք օրվան/ժամին՝ նիշքի այդ պահին տեսքը դիտելու համար։

| Օր/Ժամ | Մանրապատկեր | Օբյեկտի չափը | Մասնակից | Մեկնաբանություն | |

|---|---|---|---|---|---|

| ընթացիկ | 13:15, 17 Հուլիսի 2012 | | 960 × 720 (10 ԿԲ) | File Upload Bot (Magnus Manske) | Transfered from en.wikipedia by User:Sfan00_IMG using CommonsHelper |

Նիշքի օգտագործում

Հետևյալ 4 էջերը հղվում են այս նիշքին՝

Նիշքի համընդհանուր օգտագործում

Հետևյալ այլ վիքիները օգտագործում են այս նիշքը՝

- Օգտագործումը en.wikipedia.org կայքում

- Օգտագործումը es.wikipedia.org կայքում

- Օգտագործումը fa.wikipedia.org կայքում

- Օգտագործումը it.wikipedia.org կայքում

- Օգտագործումը ja.wikipedia.org կայքում

- Օգտագործումը ko.wikipedia.org կայքում

- Օգտագործումը vi.wikipedia.org կայքում

- Օգտագործումը zh.wikipedia.org կայքում

{kind=link}