Պատկեր:U.S. Home Ownership and Subprime Origination Share.png

{kind=link}

{kind=link}

{kind=link}

Սկզբնական նիշք (960 × 720 փիքսել, նիշքի չափը՝ 29 ԿԲ, MIME-տեսակը՝ image/png)

{kind=link}

Ամփոփում

|

This graph image could be re-created using vector graphics as an SVG file. This has several advantages; see Commons:Media for cleanup for more information. If an SVG form of this image is available, please upload it and afterwards replace this template with

{{vector version available|new image name}}.

It is recommended to name the SVG file “U.S. Home Ownership and Subprime Origination Share.svg”—then the template Vector version available (or Vva) does not need the new image name parameter. |

| Նկարագրում |

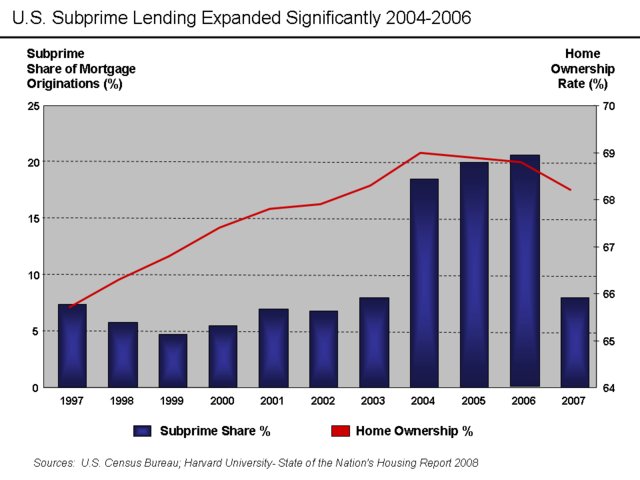

English: There are various mortgage categories defined based on the credit quality of the borrower. These include subprime, Alt-A, and Prime. The share of subprime mortgages is shown in the diagram. It is the ratio of the dollar value of subprime mortgages to all originations, expressed as a percentage. The level of home ownership is based on the percentage of American households that own homes rather than rent.

Subprime mortgages remained below 10% of all mortgage originations until 2004, when they spiked to nearly 20% and remained there through the 2005-2006 peak of the housing bubble.[1] A proximate event to this increase was the April 2004 decision by the SEC to relax the net capital rule, which encouraged the largest five investment banks to dramatically increase their financial leverage and aggressively expand their issuance of mortgage-backed securities. This applied additional competitive pressure to Fannie Mae and Freddie Mac, which further expanded their riskier lending.[2] Excerpts from the Harvard Report:

Other interpretations:

Source Data |

| Թվական | 30 Մայիս 2009 (original upload date) |

| Աղբյուր | Transferred from en.wikipedia to Commons. |

| Հեղինակ | Farcaster at անգլերեն Վիքիպեդիա |

Արտոնագրում

- Դուք ազատ եք՝

- կիսվել ստեղծագործությամբ – պատճենել, տարածել և փոխանցել այս աշխատանքը։

- վերափոխել – ադապտացնել աշխատանքը

- Պահպանելով հետևյալ պայմանները'

- հղում – Դուք պետք է նշեք հեղինակի (իրավատիրոջ) հղումը:

- համանման տարածում – Եթե դուք ձևափոխում եք, փոխակերպում, կամ այս աշխատանքի հիման վրա ստեղծում եք նոր աշխատանք, ապա ձեր ստեղծածը կարող է տարածվել միայն նույն կամ համարժեք թույլատրագրով։

|

Այս վավերագրման պատճենահանման, տարածման և/կամ ձևափոխման թույլտվություն կամ լիցենզիայի GNU FDL պայմաններով 1.2 մեկնակերպի կամ ավելի ուշ, հրատարակված Ազատ ծրագրային ապահովության հիմնադրամում, առանց անփոփոխելի հատվածների, առանց բնագիրների, որոնք տեղադրված են առաջին և վերջին շապիկներում: Լիցենզիայի պատճենը գտնվում է GNU Free Documentation License հատվածում: |

Original upload log

{kind=link}

- 2009-05-30 23:44 Farcaster 960×720× (30085 bytes)

- 2009-05-30 23:16 Farcaster 960×720× (28829 bytes) {{Information |Description = Subprime mortgage share as % originations and home ownership rate |Source = [http://www.jchs.harvard.edu/publications/markets/son2008/son2008.pdf Harvard 2008 State of Nation's Housing Report] |Date = M

Նիշքի պատմություն

Մատնահարեք օրվան/ժամին՝ նիշքի այդ պահին տեսքը դիտելու համար։

| Օր/Ժամ | Մանրապատկեր | Օբյեկտի չափը | Մասնակից | Մեկնաբանություն | |

|---|---|---|---|---|---|

| ընթացիկ | 00:57, 14 Հոկտեմբերի 2010 | | 960 × 720 (29 ԿԲ) | Hideokun | {{Information |Description={{en|There are various mortgage categories defined based on the credit quality of the borrower. These include subprime, Alt-A, and Prime. The share of subprime mortgages is shown in the diagram. It is the ratio of the dollar va |

Նիշքի օգտագործում

Հետևյալ 3 էջերը հղվում են այս նիշքին՝

Նիշքի համընդհանուր օգտագործում

Հետևյալ այլ վիքիները օգտագործում են այս նիշքը՝

- Օգտագործումը de.wikipedia.org կայքում

- Օգտագործումը el.wikipedia.org կայքում

- Օգտագործումը en.wikipedia.org կայքում

- Օգտագործումը fr.wikipedia.org կայքում

- Օգտագործումը gu.wikipedia.org կայքում

- Օգտագործումը hi.wikipedia.org կայքում

- Օգտագործումը it.wikipedia.org կայքում

- Օգտագործումը ja.wikipedia.org կայքում

- Օգտագործումը kn.wikipedia.org կայքում

- Օգտագործումը lt.wikipedia.org կայքում

- Օգտագործումը ta.wikipedia.org կայքում

{kind=link}